Molloy will oversee the organization's accounting, financial planning and analysis, reimbursement, and revenue cycle functions, as well as managed care contracting and treasury starting in July.

While his current role is still as the managing director and head of municipal banking at Citi, Molloy is not new to the innerworkings of Ochsner Health’s finances. He has been a key financial advisor to Ochsner for several years and has spent more than a decade overseeing banking for all municipal-related activity, including public finance, healthcare, higher education, and public-private partnerships.

When Molloy officially joins Ochsner in July, he will work side-by-side with Ochsner’s current CFO, Scott Posecai, who will retire as CFO in December.

Molloy recently chatted with HealthLeaders about his new role and how he plans to ensure the financial success of the organization once Posecai departs.

HealthLeaders: Ochsner says you will play a pivotal role in the continued development and execution of strategy as the health system builds on its clinical excellence and innovation in healthcare delivery. How does your background in banking make you a good fit for this new role and Ochsner in particular?

Jim Molloy: I’ve worked on all types of financings and have led numerous strategic projects over the years. This background has afforded me a strong understanding of healthcare and the financial markets while allowing me to create strong relationships with investors and other stakeholders. It has also exposed me to the strategic aspects of the business.

I have been fortunate to work with Ochsner on projects that fueled the organization’s strategic growth, including the original merger of the clinic and the foundation. I have developed a strong connection to the organization, and I understand how important Ochsner is to the overall health and well-being of the communities it serves. I have also been fortunate enough to get to know much of the executive and board leadership.

I have a deep respect for the culture and depth of talent at Ochsner, and I’m committed to the organization’s values and mission to serve, heal, lead, educate and innovate.

Photo courtesy of Ochsner Health.

HealthLeaders: CFOs need to help their organizations grow while keeping expenses low. What sort of processes do you plan to put in place to make sure this happens?

Molloy: My engineering background and my consulting work helped influence the process-oriented thinking I adopt and live by today. It is important to develop a culture in which leaders seek continuous improvement, while also measuring the appropriate things and benchmarking yourself in key areas against best-in-class organizations. While it is important to always keep a mindset toward reducing expenses, the true key to success for any organization is disciplined growth.

HealthLeaders: With your history in banking, how will you use your expertise to think outside of the box when it comes to Ochsner’s investment portfolio?

Molloy: When considering investments, it’s critical to have strong discipline and balance appropriate risk-taking.

The organization has done a great job of this over the years, but over time I will utilize my industry connections to identify new ideas and opportunities to improve.

HealthLeaders: How will you help ensure financial stability for Ochsner in 2024 and beyond?

Molloy: I will look to develop strong relationships across Ochsner’s management, clinical leadership, and finance teams to ensure we can support our operational and clinical priorities, which in turn will support our strategic growth priorities.

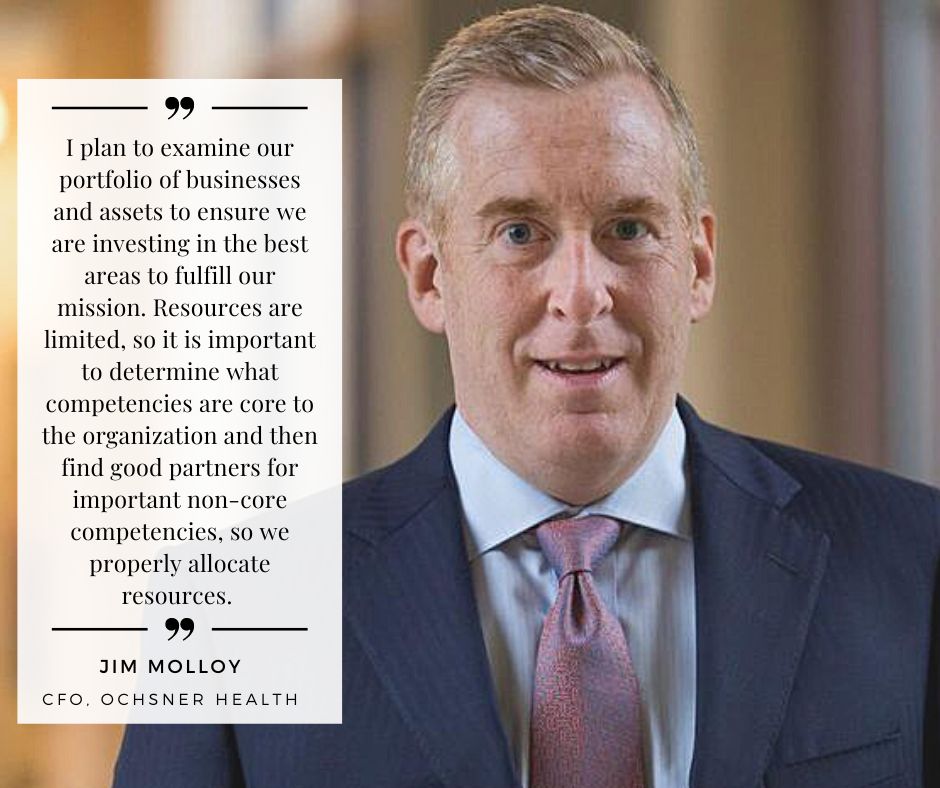

I plan to examine our portfolio of businesses and assets to ensure we are investing in the best areas to fulfill our mission. Resources are limited, so it is important to determine what competencies are core to the organization and then find good partners for important non-core competencies, so we properly allocate resources.

Most critically, we must keep our focus on better serving our patients and improving the lives and the health of our communities. We need to find new ways to make healthcare more accessible to the communities we serve, and work to ease the pressures on our workforce. Improving in those arenas each year will be critical to our success.

HFMA announced the winners of its 2023 MAP Award for high performance in revenue cycle, and 10 hospitals were awarded.

According to the Healthcare Financial Management Association (HFMA), there are five physician practices, four hospital systems, three individual hospitals, two critical access hospitals, and one an integrated delivery system, with high performing revenue cycles.

The awards were presented at the HFMA annual conference on June 25 in Nashville and recognized providers that have excelled in meeting industry standard revenue cycle benchmarks, implemented the patient-centered recommendations, achieved outstanding patient satisfaction, and more.

Some of the winners of HFMA’s 2023 MAP Award for high performance in revenue cycle include the following organizations:

Winning integrated delivery system:

Saint Francis Health System

Winning hospital systems:

Ballad Health

Covenant Health

OhioHealth

ThedaCare

Winning individual hospitals:

CHRISTUS St. Michael Health System

Liberty Hospital

The University of Texas MD Anderson Cancer Center

Winning critical access hospitals:

Henry County Health Center, Inc.

Van Diest Medical Center

Winning physician practices:

Alo/Avance Care

ENT and Allergy Associates

Graves-Gilbert Clinic

Heart and Vascular Care

State of Franklin Healthcare Associates

“We are truly honored to be recognized with this high-performance award,” Steven Sinclair, CFO of Graves-Gilbert Clinic, told HFMA. “While our tradition of clinical excellence dates back more than 85 years, our approach to revenue cycle could not be more contemporary. Our entire revenue cycle team is dedicated to making the financial experience a seamless one for our patients.”

The new codes cover a range of procedures, including:

Bypass femoral artery using conduit

Insertion of conduit to short-term external heart assist system

Insertion of intraluminal device, bioprosthetic valve

Introduction of drugs into peripheral veins

Repositioning of larynx

The revisions and deletions mainly featured vertebral fusion procedures and introduction of certain drugs.

When it comes to outpatient reporting, most of the HCPCS code changes will be implemented July 1, but some codes were made available as early as March 14.

New administration code 0174A is for patients six months through four years of age and is to be used in conjunction with CPT product code 91317 (SARS-CoV-2 vaccine, mRNA-LNP, bivalent spike protein, preservative free, 3 mcg/0.2 mL dosage, diluent reconstituted, tris-sucrose formulation, for intramuscular use). In March, the Food and Drug Administration amended the bivalent Pfizer-BioNTech COVID-19 vaccine’s emergency use authorization to allow clinicians to administer a booster to certain young patients. Shortly after, the AMA released administration code 0174A, which became effective March 14.

The transmittal also mentioned the 20 Category III CPT codes that were originally introduced in January. These 20 Category III CPT codes will be available for use beginning July 1.

All of these new procedure codes come in conjunction with the 2024 ICD-10-CM diagnosis codes that were announced in June.

Robust data is critical to hospitals’ efforts to improve reimbursement. One way to better capture data on your patient populations is through proper documentation and keeping revenue cycle staff up to date on code changes.

June's National Hospital Flash Report from Kaufman Hall says hospital finances showed signs of stabilizing in a few key areas in May.

Healthcare leaders have been battling incessantly against poor operating margins and increases in expenses. But luckily for health systems such as Ascension Healthcare—who recently announced "significant improvement plans" focused on operational efficiencies and controlling expense growth amid a loss of almost $1.8 billion—stabilization may be on the horizon.

According to the June 2023 report, hospital finances saw slightly improved operating margins, declining labor expenses, and increases in outpatient visits, i.e., more reimbursement.

Here are three ways hospitals saw financial improvement in May:

Operating margins regain positive territory.

The median year-to-date (YTD) operating margin index for hospitals was 0.3% in May, up slightly compared to 0.1% in April and March, the report says.

Although operating margins are slowly regaining positive territory, they are well below levels during the latter half of 2021 and prior to the pandemic.

Labor expenses saw a decrease.

While labor costs remain significant, expenses were down 9% in May 2023 compared to May 2022. FTEs per AOB saw a decrease of 6% between May 2022 and 2023, and a decrease of 21% compared to May 2020.

Interestingly, April’s report showed that high expenses continued to put pressure on hospitals, with labor expense per adjusted discharge increasing 3% from March to April, that report revealed.

More hospital revenue is being driven by outpatient services.

Net operating revenue per calendar day was 9% higher in May 2023 compared to May 2022, while outpatient revenue per calendar day rose 14% over the same time frame.

“Now that hospital finances are showing signs of stabilization, it’s an opportune time for executives to reevaluate their longer-term business strategy,” Erik Swanson, senior vice president of Data and Analytics with Kaufman Hall, said in a statement.

“The continuing shift in patient demand from inpatient to outpatient services is particularly important and will inform business decisions for years to come,” he said.

The June 2023 National Hospital Flash Report draws on data from more than 1,300 hospitals from Syntellis Performance Solutions.

The president of St. Johns Radiology Associates talks about its middle revenue cycle tech implementation process.

Implementing new technology to reduce administrative burdens and increase bottom lines is commonplace in the revenue cycle, but getting there isn’t always an easy road.

Between administrative buy-in and complicated go-lives, there always tends to be hiccups from conception to implementation. But this is where St Johns said its experience differed.

Just like other healthcare organizations, St. Johns needed to streamline revenue cycle processes. The group decided to do this by implementing an advanced speech reporting solution with built-in computer-assisted physician documentation functionality for its middle revenue cycle.

HealthLeadersrecently chatted with Dr. Arif Kidwai, president of St. Johns Radiology Associates, about the steps the organization took when implementing an AI-powered clinical documentation and workflow management solution and how it was able to avoid any major hurdles in execution.

HealthLeaders:Healthcare organizations have had a rough few years financially as they try to navigate inflation and labor shortages, among many other challenges, so this has led to a lot of leaders in your position to look toward technology to fill gaps and help their bottom lines. Can you tell us about the gaps that you were seeing at your organization and what technology you implemented to help fill those gaps?

Dr. Arif Kidwai: Yes, the last two to three years have been really rough for everybody in the healthcare industry across the board, radiologists included.

I've been fortunate to be a part of a hospital system where the executives are very proactive and ahead of the curve. They've always been aggressive with looking at new technology and trying to find ways to deliver healthcare more efficiently and provide better care for the patients.

About ten years ago, we started moving towards creating a better workflow within our own department and part of that process was to look for a new voice recognition system. At that time, we looked at a lot of the major players. But then we came across the 3M Fluency for Imaging product. For us, that was a game changer.

Once we started using a better workflow with a better voice recognition system, we were able to improve our turnaround times in radiology so that we had faster reports coming out to the clinic patients. We now have better accuracy in our reports because the voice recognition technology is the best that we've ever seen.

Having that voice recognition technology with a better workflow package made us better radiologist's both in quality and in our efficiency. Its something that we've seen now play out positively in the last three years, especially as things have even been more tight in the industry as the number of radiologists relative to the number of cases that we see annually has continued to grow and grow and grow.

There’s a great data graph out there that shows this gap between the increasing imaging volume year over year versus the relative flat number of radiologists that we've had nationally. And it's a challenge for everybody you know, as patient volume continues to grow and the shortage of clinicians persists. I think just finding that efficiency and the technology has been the only way to cope with that.

HealthLeaders: I know you said you're a part of a larger health system, so did you have to get an ample amount of buy-in from others in the system when it came to which solution you wanted to adopt?

Kidwai: We were really fortunate. When we were going through this process our chief medical information officer came to us and said the hospital organization wanted to buy one vendor product that would provide voice recognition software both in the radiology arena as well as hospitalwide for the new EMR that they were purchasing.

He came to me and said, ‘you know, at the end of this, it's the radiologists’ decision. You tell us what you like, and the hospital will follow.’ So, we worked hand-in-hand with his team, and we brought in all the major players at the time and we went through the standard inner product review of product demos.

For us, it was an easy decision. We had an ‘open mic night’ of sorts because our executives basically sat down in a room and had all the radiologist come in one by one. We came in, sat in the chair, and dictated into the microphone—signed in under a generic account with no voice training—and we just watched it work. It was really refreshing because technology before that had really been lagging as far as the radiologist expectations.

Everybody knew the pain of trying to correct reports, and to be able to sit down just see it work was really the thing that changed everybody's attitude about moving forward with new technology. That night we basically had a unanimous vote from the radiologists that this was the tech we wanted.

We went to the CMIO the next day and said, ‘this is our choice,’ and he smiled. He said, ‘that was my choice to, I just didn't want to tell you.’ That's how we as an organization came to this decision, and then we moved forward with it.

HealthLeaders: I frequently hear from other leaders that new technology is great, but implementation isn't always the easiest. So now that you’re over that hurdle, can you tell us a little bit about how implementation went at your practice and how you overcame any obstacles?

Kidwai: Yes, adoption of new tech is always a challenge for everybody. But prior to go-live our vendor did a lot of prep with our team. They did lot of training for our IT department. They came and they coached the radiologists of what to expect. Then on the go-live date they had trainers on site. We had both of our major sites covered with staff.

We also already had IT people that had been trained, so we were all ready for it. We also purposely decreased our outpatient volume for two days just to kind of handle the change and knowing that there would be a little bit of a kind of a learning curve to this.

But, for us, the shock was that after about three days, we were back to 100% productivity. And so, everybody went from being afraid of what's going to happen to three days later just simply doing our jobs again and forgetting that we had to go through this learning curve.

The CFO of Brightside Health talks financial strategy amid a telehealth boom.

CFOs know that COVID-19 changed the game completely—not only from a financial lens but from a strategy perspective as well.

Traditionally, there has been hesitance to adopt telehealth due to reimbursement issues. Reimbursement is still a hinderance, especially with the pandemic waivers expiring and some payers reluctant to expand coverage, but the curtain has been lifting and the barrier to access is shrinking.

Now, it’s not uncommon for organizations to implement a virtual care road map across the care continuum as a lower-cost, more productive option for care delivery. As strategy shifts, we are seeing the creation of more orginizations that specialize in 100% virtual care.

From a cost perspective it can seem like a no-brainer, but without a mature telehealth strategy, the implementation of a 100% telehealth service may encounter resistance from all corners—IT, billing, clinical teams, and even patients. On top of this, the numerous downstream consequences for failing to financially plan are vast.

Chris Murray, the new CFO at Brightside Health—a completely virtual, mental health provider organization, is well aware of the risks, but a solid telehealth understanding and financial strategy is the key to success, Murray says.

Murray recently chatted with HealthLeaders about the organization’s financial strategy along with the three main differences he sees between the financial strategy of a completely virtual provider organization versus that of a brick-and-mortar provider.

HealthLeaders: You have over 15 years’ experience in roles across finance, operations, and go-to-market functions at healthcare and technology companies, so what drew you to the CFO role for Brightside Health?

Murray: The current spotlight on mental healthcare is critical, especially as one in five Americans live with some form of mental illness. Like many of us, mental health issues have touched my family personally. My passion for changing the way the healthcare industry evolves to meaningfully support people living with severe depression and anxiety aligns with the mission of Brightside Health to deliver life-changing mental health care to everyone who needs it.

I’ve been in the CFO role at Brightside Health for a few months now, and I truly believe our solutions are changing people’s lives for the better. I am excited to see what the future holds for Brightside Health and how I can help grow the business.

HealthLeaders: What direction do you plan to take Brightside’s financial strategy?

Murray: The financial strategy for Brightside Health is exciting and complex. Because we work with many different markets, there’s opportunity to grow the revenue stream in a variety of ways. We’re driving momentum in the commercial market among payers, providers, and even employee assistance programs and are exploring other avenues such as Medicare and Medicaid, while still serving consumers directly. We know each stakeholder presents a unique opportunity and plan to examine how their differentiators fit into our broader mission and vision, while also addressing their financial objectives.

HealthLeaders: 100% virtual care is a relatively new concept, so how do you plan to drive growth and strategic initiatives?

Murray: An important role of a CFO is to build an infrastructure that supports the efforts of our product and technology teams. To do this we need robust performance tracking in place to ensure we’re monitoring progress against our objectives and putting numbers and structure to our challenges and successes. My team and I will also continue to analyze where there’s whitespace in the competitive landscape, working to identify areas that are primed for innovation that Brightside Health can play a key role in.

HealthLeaders: How does building a financial strategy for a digital-first mental healthcare provider differ from building a plan for a hospital or health system?

Murray: There are three differences that come to mind when thinking about our financial strategy versus that of a brick-and-mortar provider.

The first is the difference in compliance and legal requirements. As a mental healthcare provider, we must think about state-by-state licensing for our therapists (in all 50 states plus D.C.) whereas health systems typically work in one or a handful of states and don’t need to be mindful of local laws and regulations.

The second is infrastructure. We don’t have brick-and-mortar costs, which means much less overhead and ultimately allows us to treat more patients.

Third are the marketing costs–essentially how we reach people and how people can find us virtually. Traditionally, this isn’t something that a hospital or health system has to think about as there’s already awareness of the physical location (and often less options within the community to select from). Building brand awareness and ensuring our key differentiators are well known in the industry and among potential patients is a critical function of our business and something we are implementing in a meaningful way.

HealthLeaders: From a financial perspective, what do you see for the future of telehealth over the next few years?

Murray: The industry has no doubt been accelerated by the pandemic, and telehealth has proven to be a viable solution that will continue to be the future of healthcare. Traditionally, there has been hesitance to adopt telehealth due to reimbursement issues, but since the pandemic, the curtain has been lifted and the barrier to access has been removed. We’ve seen patients express the desire and interest to stick with telehealth, especially for behavioral healthcare. I think we’ll see increased demand across the industry to adapt and implement more telehealth solutions into platforms because that friction no longer exists.

Prepare your revenue cycle teams for several hundred new fiscal year 2024 ICD-10-CM codes now finalized to take effect October 1.

CMS recently announced the addition of 395 new diagnosis codes, 25 deletions to the diagnosis code set, and 13 revisions. An ample amount of these changes pertains to reporting certain diseases, accidents and injuries, and social determinants of health (SDOH). As mentioned, these code updates will take effect on October 1.

The new diagnosis codes are spread throughout the code set, with several dozen pertaining to osteoporosis with fractures, retinopathy and muscle entrapment in the eye, and disease of the nervous system—including Parkinson’s disease and epilepsy.

For example, the final update confirms the introduction of five new codes for Parkinson’s disease:

G20.A1, Parkinson’s disease without dyskinesia, without mention of fluctuations

G20.A2, Parkinson’s disease without dyskinesia, with fluctuations

G20.B1, Parkinson’s disease with dyskinesia, without mention of fluctuations

G20.B2, Parkinson’s disease with dyskinesia, with fluctuations

G20.C, Parkinsonism, unspecified

Of the 395 new codes, 123 of them reside in the external causes of morbidity chapter of the ICD-10-CM manual, specifically new codes to capture accidents and injuries.

When it comes to SDOH, there are 30 new diagnosis codes for factors influencing health status and contact with health services. There are also a host of new guidelines for reporting these codes.

For example, there is a new code for reporting an encounter for HIV pre-exposure prophylaxis. A “code also” note instructs coders to report risk factors for HIV, when applicable.

An extensive “code also” update for “other specified problems related to upbringing” says codes for the following diagnoses should also be reported when applicable:

Absence of a family member

Disappearance and death of family member

Disruption of family by separation and divorce

Other specified problems related to primary support group

Other stressful life events affecting family and household

This 2024 diagnosis code update comes at a time when hospitals and health systems are working more diligently than ever to address their patients’ social needs and the broader SDOH in the communities they serve.

Robust data related to patients’ social needs is critical to hospitals’ efforts to improve the health of their patients and communities. One way to capture data on the social needs of patient populations is through proper documentation and keeping revenue cycle staff up to date on code changes, which will help to better identify non-medical factors that may influence a patient’s health status.

CMS recently launched a new consumer webpage for the No Surprises Act.

CMS launched a webpage for consumers detailing patient protections from unexpected out-of-network medical bills under the No Surprises Act.

The website also addresses the dispute resolution process for uninsured and self-pay patients interested in disputing their bill based on a provider’s good faith estimate.

Surprises bills continue to be sprung on patients, even with a federal ban in place, with one in five adults receiving an unexpected medical charge this year, according to a survey by Morning Consult.

As revenue cycle leaders know, the No Surprises Act is meant to protect patients from receiving unforeseen bills for out-of-network and emergency services after receiving treatment, yet 20% of respondents in the survey say they or their family have been charged unexpectedly, with another one in five billed after being treated by an out-of-network provider at an in-network facility.

The bills have been especially costly in some cases, as 22% of respondents say their charges were over $1,000.

Creating more resources for patients, such as CMS’ webpage, could help patients better understand the law and what to expect when receiving care.

A bipartisan group of over 30 senators penned a letter to CMS asking the agency to reevaluate the 2024 inpatient payment rate.

The recent letter sent to CMS, led by Sens. Robert Menendez (D-N.J.) and Kevin Cramer (R-N.D.), informs the agency of concerns that the payment rate increase put forward in the fiscal year (FY) 2024 inpatient prospective payment system (IPPS) proposed rule will actually result in an overall payment reduction for hospitals.

According to the letter, in the FY 2024 IPPS proposed rule CMS relies heavily on data that does not account for the impact of the current elevated costs and expenses in providing healthcare. The senators also pointed out that the productivity update in this proposed rule assumes that healthcare facilities can replicate the general economy’s productivity gains.

“However, the critical financial pressures that hospitals and health systems continue to face have resulted in productivity declines, not gains,” according to the letter.

Each year, CMS is required to update payment rates for IPPS hospitals using the hospital market basket index to account for price changes in goods and services. To ensure Medicare payments more accurately reflect the cost of providing healthcare today, the senators asked CMS to use its special exceptions and adjustments authority to make a retrospective adjustment to the FY 2022 market basket update.

Unsurprisingly, the American Health Association (AHA) is backing the Senators’ letter.

“The AHA thanks Senators Menendez and Cramer for leading this important bipartisan effort urging CMS to ensure hospitals and health systems have the resources they need to continue delivering high-quality care to their patients and communities,” Lisa Kidder Hrobsky, AHA’s senior vice president for advocacy and political affairs said in a statement.

“This support is more needed than ever as the hospital field continues to confront rising inflation, workforce shortages and surging costs for supplies and drugs,” Kidder Hrobsky said.

Earlier this year, the AHA penned its own statement to CMS saying the association was “deeply concerned with CMS’ woefully inadequate proposed inpatient hospital payment update.”

According to CMS, under the FY 2024 IPPS proposed rule, acute care hospitals that report quality data and are meaningful users of EHRs will see a net 2.8% increase in payments in FY 2024 (compared to 2023). However, disproportionate share hospitals could be facing a payment cut of $115 million.

The national healthcare expenditure topped $4.4 trillion in 2022.

Now may be the time to assess your organization’s financial future as healthcare spending is growing, so much so that the United States spent $4.4 trillion on healthcare in 2022, a growth rate of about 4.3%, according to a federal estimate released today.

That rate of growth is projected to average 5.4% annually through 2031, according to Centers for Medicare and Medicaid Services’ (CMS) estimates put forward in a new study published in Health Affairs.

Despite that robust rate of growth, healthcare spending in 2022 is not expected to keep pace with overall economic growth in the United States, and healthcare’s share of the gross domestic product in 2022 is expected to fall from 18.3% to 17.4%, CMS says.

However, that trend is not expected to last. GDP growth through 2031 is projected to average 4.6% annually—0.8% lower than the average growth in national health expenditures—which means that health spending will hit 19.6% of GDP by 2031, CMS says.

“Altogether, and consistent with its past trend, health spending for the next ten years is expected to grow more rapidly, on average, than the overall economy,” says Sean Keehan, an economist in the Office of the Actuary at CMS, and the Health Affairs study’s first author.

The projections could spell trouble for providers.

As we know, when national health spending growth increases, reimbursement rates may not keep up, which means hospital leaders may have increased expenses while receiving less revenue. Now is the time to consider strategic decisions regarding the allocation of resources, managing expenses, and revenue growth.

CMS also says Medicare spending growth is projected to accelerate from 4.8% in 2022 to 8% in 2023, with expenditures expected to exceed $1 trillion, despite the end of the public health emergency in 2023 and the associated expirations of the skilled nursing facility 3-day rule waiver and the 20% payment increase for inpatient COVID-19 admissions.

Payers will be feeling the squeeze as well. Among the major payers, Medicare spending is expected to grow the fastest over the course of 2022-201 as the last of the baby boomers enroll in the program through 2029, the report says.

Private health insurance spending is expected to grow 5.4% annually, whereas Medicaid’s average rate of spending growth is projected to be 5.0% during the same period.

Hospital spending is expected to grow more quickly on average (5.8%) than average spending growth for physician and clinical services (5.3%), and prescription drugs (4.6%) during this timeframe.

Similarly, the report says the average price growth for hospitals (3.2%) is projected to be greater than that of prescription drugs (2.2%) and physician and clinical services (2.0%).

According to the report, businesses, households, and other private revenues are expected to pay the same proportion of total health spending in 2031 as they did in 2021 (51%). Government spending is projected to account for the remaining 49% (also the same as 2021). Before the pandemic, in 2019, those shares were 54% and 46%, respectively.