Sanford Health System's new CFO will be facing challenges head on by investing in multiple areas of the business.

Low reimbursement, staffing shortages, low patient volumes, regulatory barriers, and COVID-19 disruptions all played a role in the shuttering of 136 rural hospitals between 2010 and 2021, including a record 19 closures in 2020.

Unfortunately, a lot of these challenges have not let up as rural hospitals contend with rising costs for labor, inflationary pressures, and more.

For these reasons and more, Sanford Health System, the largest rural health system in the United States, faces a unique set of financial challenges that make serving the small communities in which they operate more difficult than their larger counterparts.

To hear how Sanford’s new CFO Scott Wooten plans to address these challenges, I chatted with him on the third day in his new role. By placing a focus on its investments and long-term success and stewardship, Wooten is confident in Sanford’s financial future.

Scott Wooten, former CFO at both Baptist Health and AdventHealth, has big plans for financial success in his new role.

Sanford Health, the largest rural health system in the United States, recently tapped Scott Wooten, FACHE, MBA, as its CFO following a comprehensive national search process, but the financial landscape he is stepping into won’t be without its hurdles.

As we know, rural health systems like Sanford face a unique set of financial challenges that make serving the small communities in which they operate more difficult than their larger counterparts.

But, Wooten told me on the third day in his new role, between building relationships with his new team and placing a focus on its investments and long-term success and stewardship, he is confident in Sanford’s financial future.

“Sanford Health is an incredible organization,” Wooten said. “It has a strong team, and my job is to support the team in implementing the current plans that are already in place first and foremost,” he says.

From there, Wooten says he plans to begin to look more long-term and examine how Sanford will grow and invest.

Pictured: Scott Wooten, CFO of Stanford Health. Photo courtesy of Sanford Health.

"For example, right now we're investing huge in automation and AI to streamline how we do our work. We're also making investments in the future models of care," he says. "This includes a very large investment in virtual care to ensure that we can continue to provide access to world class healthcare in rural areas."

On top of this, Sanford is also looking at growing in the ambulatory and outpatient space.

In addition, Sanford will be making investments in growing its workforce—specifically in its graduate medical education (GME) program. “We will be adding 15 new programs to make it a total of 27 GME programs by 2027. Then, we'll have over 300 fellows and residents coming out of those programs,” Wooten says.

What comes hand-in-hand with investments, though, is capital.

Luckily for Sanford, Wooten, a seasoned finance leader with deep experience in the nonprofit healthcare sector, previously served as CFO at Florida-based Baptist Health for eight years. Wooten also held executive finance roles with Alegent Creighton Health in Nebraska, AdventHealth Central Florida, and AdventHealth North Texas.

The financial expertise he gained in those roles will help to foster the financial success of his new organization.

“What I’ve learned is every market is different, and every culture is different, so what we're going to focus on is long-term success and long-term stewardship here at Sanford,” Wooten says. “And to do that, a person needs to focus on what their balance sheet will look like in the future and then strategize on how to get there from a strength perspective.”

“In addition, that long-term stewardship sometimes creates different conversations, and Sanford has tremendous forward-looking structures in place. We're just going to align those a little bit and have some additional conversations about where we want to be in the future, both physically as well as from a balance sheet perspective,” Wooten says.

CVS Health announced a new CFO, a move that signals its commitment to adapting to market dynamics and staying ahead of the competition.

In a strategic move, CVS Health has officially named Tom Cowhey as its permanent CFO marking a significant development in the healthcare industry.

The appointment comes after Cowhey successfully held the interim CFO role since late last year, stepping in for Shawn Guertin, who served as CFO and president of health services.

The shift in leadership at CVS Health is poised to have a profound impact on the healthcare market, particularly on hospitals and health systems that view CVS Health as a major disruptor to their traditional business models.

But why does the appointment matter to other healthcare CFOs?

Cowhey could give your finance strategies a run for their money as his past brings a wealth of financial executive experience from roles in both provider and payer companies. Prior to his tenure at CVS, Cowhey served as CFO of Surgery Partners and held key positions in strategy and finance at Aetna.

His diverse background positions him to navigate the complex nature of the healthcare industry and will bring an interesting dynamic into the payer/provider landscape.

Speaking of payers, CVS Health's announcement also sheds light on its optimistic outlook for its Medicare Advantage (MA) plans.

The company anticipates surpassing its previous targets for 2024, with an expected addition of at least 800,000 new MA members. This positive forecast is attributed to growing sales and member retention, showcasing CVS' resilience and strategic positioning in the highly competitive MA landscape—and one that has been quite complex as of late.

As CVS Health continues to evolve and adapt to the dynamic healthcare market, Cowhey's leadership as CFO becomes pivotal in driving financial strategies that will shape the company's trajectory.

The ripple effect of these changes is likely to be felt across the industry, influencing the strategies of other healthcare CFOs as they navigate a landscape marked by innovation, competition, and evolving consumer expectations.

Healthcare CFOs know the pandemic cost them big, but now there's a number attached for one state.

After years of tight margins made worse by the pandemic, many hospitals are beginning to feel a measure of relief. But how much financial strain did the pandemic really put on hospitals and health systems?

In Pennsylvania, it was $8.1 billion worth of strife.

You read that right. The total COVID-19 related expenses and lost revenue reported by Pennsylvania hospitals and health systems between January 2020 and December 2022 were $8.1 billion, according to the report by The Pennsylvania Health Care Cost Containment Council and The Hospital and Healthsystem Association of Pennsylvania.

While this report only spotlighted Pennsylvania, there are a few key insights that are applicable to CFOs nationwide.

So what was the true financial impact?

As mentioned, Pennsylvania hospitals and health systems reported a staggering $8.1 billion in total COVID-19-related expenses and lost revenue during the pandemic.

Although most hospitals and health systems remained financially stable due to COVID relief funds, those funds have since dried up while the same challenges still exist.

Of this sum, COVID-19 staffing costs emerged as the most significant expenditure, reaching $1.3 billion. According to the report, other costs included:

Testing expenses: $374 million

Supplies and equipment expenses: $679 million

Construction expenses: $28 million

Housing care expenses: $9 million

Other expenses: $434 million

Revenue loss: $5.3 billion

When it comes to the staffing costs, the amount highlights the immense financial strain incurred by hospitals in responding to the staffing demands posed by the pandemic. CFOs still need to scrutinize these figures to gain a nuanced understanding of where financial resources were concentrated and explore avenues for financial resilience moving forward.

The report also shed light on how the pandemic has exacerbated workforce shortages in Pennsylvania's healthcare sector.

Hospitals reported an average statewide vacancy rate of over 30% for key clinical positions, such as registered nurses, nursing support staff, and medical assistants, by the end of 2022.

This intensification of workforce shortages continues to pose an ongoing challenge to hospitals, hindering their ability to provide comprehensive care and potentially impacting patient outcomes. And as we know, these staffing shortages have been the catalyst to the increasing number of workforce strikes.

As mentioned, CFOs must strategize to address staffing shortages, focusing on recruitment, retention, and workforce optimization.

But what about other states?

A previous study showed that COVID-19 care prompted higher operating expenses and rapidly escalating labor costs for CFOs nationwide. In fact, hospitals in the United States experienced a total loss of over $200 billion because of an estimated 45% decrease in operating revenue just between March and June of 2020.

Pennsylvania's data through 2022 gives healthcare CFOs across the nation a granular look into these costs, providing valuable insights into the continued long-term financial repercussions of the pandemic.

The report's focus on COVID-19-related expenses and lost revenue underscores the continued need for robust financial planning and risk management, especially as many CFOs are still clawing their way out of the red.

CFOs should conduct thorough audits of their institutions' pandemic-related financial data, identifying areas for potential cost containment and revenue enhancement. Leveraging data can not only assist CFOs in forecasting future financial scenarios and implementing proactive measures, but help them push their current margins in the right direction.

The CFO of Montage Health detailed three financial priorities for his hospital.

CFOs need to remain vigilant in their financial planning, and Matt Morgan, MBA, FACHE, FHFMA, CFO of Montage Health’s Community Hospital, will be doing this by prioritizing three key items for his hospital.

From growing responsibly to evaluating capacity, one CFO has a few financial priorities for his hospital this year.

The median calendar year-to-date operating margin index for hospitals is reflecting an ongoing improvement, however, leaders are not off the hook.

CFOs need to remain vigilant in their financial planning, and Matt Morgan, MBA, FACHE, FHFMA, CFO of Montage Health’s Community Hospital, will be doing this by growing responsibly, evaluating capacity, and focusing on performance improvement.

How will Morgan get this done? Read on to find out.

Community Hospital is part of Montage Health—a locally owned, nonprofit network of healthcare providers with more than 250 hospital beds and 28 skilled nursing beds located in Monterey County, California.

The hospital is currently growing certain service lines to better serve its community and region, Morgan says.

So, supporting that clinical growth with key decisions on infrastructure, funding, staffing, and performance monitoring will be critical to its financial success.

On top of growing responsibly, Community Hospital also plans to evaluate its capacity.

“The hospital’s occupancy rates continue to climb, and forward projections suggest continued pressure on existing capacity,” Morgan says. “As CFO, active participation in evaluating service needs, structural design, patient throughput and capital forecasts are significant efforts in 2024.”

Performance improvement is also top of mind for Morgan.

“While volume and revenue growth has been excellent these past five years, forward projections suggest that cost growth may exceed revenue growth,” he says.

This means that continued detailed evaluation of performance improvement at the hospital, medical group, urgent care, and insurance settings is paramount Morgan says.

“Past financial success is not always indicative of future results!”

CFOs meticulously sift through quarterly earnings reports, but what do the results from some of the biggest in the nation tell us about the overall trends?

Now that health system financial results for the third quarter and first nine months of 2023 have all come in, it gives CFOs a chance to examine the overall trends.

With many making improvements on the back of some challenging financial years, operating losses, high expenses, and labors costs still weighed heavy on some of the biggest health systems in the nation—meaning these issues were surely exacerbated for smaller hospitals.

Several healthcare systems, such as CommonSpirit and Community Health Systems, reported increased operating losses compared to the previous year. This trend indicates continued financial challenges and the need for cost management strategies.

Revenue growth.

Despite the challenging financial environment, many healthcare systems, including Trinity Health, Christus Health, and HCA Healthcare, reported an increase in operating revenue. This suggests that there is potential for generating more income, although it is crucial to control expenses to improve overall profitability.

Higher expenses.

Most healthcare systems experienced an increase in expenses, particularly in terms of employee compensation and benefits, as well as supply costs. Hospital CFOs should closely monitor expense growth and implement strategies to manage costs effectively.

Net income fluctuations.

Net income varied among the healthcare systems analyzed. While some, like Kaiser Permanente and Universal Health Services, reported an increase in net income, others, such as Renton-based Providence, experienced larger operating losses. CFOs should focus on optimizing revenue streams and managing expenses to drive positive net income.

Impact of investments.

CommonSpirit and Providence reported significant net investment losses, impacting their overall financial performance. CFOs should carefully evaluate investment strategies and their potential impact on the organization's financial health.

Operating margin changes.

Tenet Healthcare reported a decrease in operating income, resulting in a decline in the operating margin. Hospital CFOs should monitor and analyze their organization's operating margin to ensure financial stability and sustainability.

Positive financial performance.

Despite the overall challenging environment, some healthcare systems, including Christus Health and Mayo Clinic, reported improved operating income and net income. CFOs should study the strategies employed by these organizations to identify potential best practices.

Providence and Mayo Clinic reported higher expenses due to wage increases. Hospital CFOs should pay special attention to labor costs and develop strategies to manage these expenses effectively.

As for the future? Not much is changing in terms of strategy. Hospital and health system CFOs need to continue to focus on optimizing revenue, controlling expenses, monitoring investments, and implementing cost management strategies to navigate the complex financial landscape.

While this news shouldn’t shock CFOs, longer-range capital plans and strategic investments will still need to be of focus. In fact, S&P says that additional spending or debt issuances could be a factor influencing credit quality, depending on balance-sheet strength and the level of cash flow improvement.

Here are nine takeaways from the report that hospital and health system CFOs should take into consideration this year.

Labor expenses remain a major challenge:

Ongoing cash flow margin pressures are primarily due to labor expenses.

The slow easing of labor expense pressures is complicated by factors such as union activity, regional market difficulties, higher base labor rates, and challenges in international recruitment.

CFOs should focus on accelerating revenue growth, improving staffing efficiencies, and making non-labor expense reductions to enhance earnings and cash flow.

Potential impact on credit ratings:

The negative sector view is influenced by the strain on cash flow, with labor and other inflationary expenses contributing to ongoing challenges.

Credit rating performance will depend on revenue trends and management's ability to achieve offsetting efficiencies.

CFOs need to closely monitor credit quality trends, with a particular emphasis on the pace of margin recovery and the ability to improve operating performance.

Balance sheet considerations:

While balance sheets remain sound, they have not strengthened materially for most organizations.

CFOs may face reduced balance-sheet flexibility as they consider capital needs and spending strategies, especially if they restart deferred capital projects or utilize debt.

Strategic spending should be carefully managed to avoid additional pressure on the balance sheet and increased carrying costs.

Varying credit quality trends:

There is a higher percentage of negative outlooks across credit ratings, with ongoing uncertainties in credit stability.

Organizations in demographically favorable regions, with healthy demand, market positions, and favorable payer rates, are more likely to perform in line with rating expectations.

Cash flow recovery in 2024 will be a crucial factor influencing credit quality assessments.

Challenges for lower-rated entities:

Lower-rated entities may face a difficult 2024 without meaningful partnerships or improved labor conditions.

Sustained higher interest rates, tighter lending, and limited debt capacity could impact capital spending for lower-rated organizations.

CFOs of lower-rated entities should seek strategies to address ongoing covenant issues and strengthen their financial positions.

Industry-specific challenges:

Revenue is strained by payer and service mix dynamics, with challenges in governmental payments, Medicaid, and commercial payer rates.

CFOs should navigate the shift from inpatient to outpatient services, manage commercial payer relationships, and address difficulties in claims processing and denial rates.

Efficiency focus and operating model improvement:

Management teams are accelerating expense management initiatives to lower the cost base.

Outsourcing to third parties, increased use of AI, asset sales, service line consolidation, and reduction in operating leases are strategies to improve efficiency.

CFOs should assess these initiatives based on cash flow, growth potential, and diversification of the revenue base.

Capital spending and debt issuance challenges:

Debt issuances have slowed, but CFOs must balance the need for capital spending with rising interest rates and weaker operating performance.

Access to capital may be difficult for lower-rated entities, potentially putting them at a long-term strategic disadvantage.

CFOs should consider less cash-intensive strategies and carefully manage debt-like structures, such as operating leases.

Event risks and ongoing pressures:

Cybersecurity events, weather, and other physical risks pose ongoing pressures on organizations.

CFOs should allocate resources for planning and investment to minimize financial and operating disruption from unexpected events.

Event risks could impact financial and management resources, affecting performance improvement needed to maintain credit ratings.

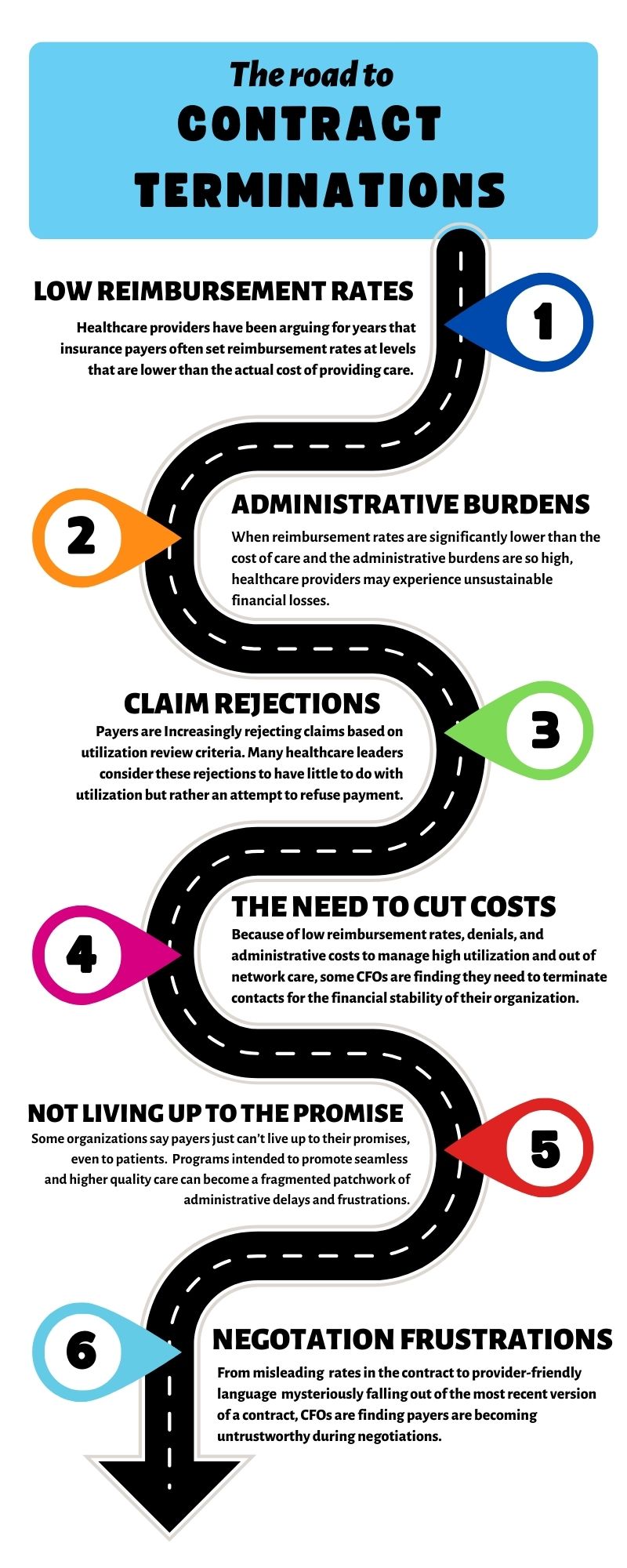

There are six major challenges that are forcing CFOs to pull the plug on payer contracts.

The payer/provider battle is raging, and signaling what may be an emerging trend: More organizations are fighting back against payers by terminating their contracts completely.

What exactly has led to the turmoil? CFOs say the reasons are vast, but below are six reoccurring challenges shared to HealthLeaders by hospital and health system CFOs and CEOs.

The great termination? More organizations are terminating payer contracts amid heated negotiations, and Medicare Advantage is in the hot seat.

The payer/provider battle is raging, and signaling what may be an emerging trend: More organizations are fighting back against payers by terminating their contracts completely, and Medicare Advantage (MA) has seemingly been the focus.

Thanks to record inflation and operational challenges, hospital and health systems find themselves with their backs against the wall in negotiations, leading CFOs to initiate contract terminations.

But what exactly has led to the turmoil? CFOs say the reasons are vast.

“Bad behavior.”

More organizations are now considering contract terminations due to dissatisfaction with reimbursement rates and overall bad payer behavior.

Healthcare providers have been arguing for years that insurance payers often set reimbursement rates at levels that are lower than the actual cost of providing care. Couple this with skyrocketing inflation costs and labor expenses, and providers can be left with no other choice.

When reimbursement rates are significantly lower than the cost of care and the administrative burdens are so high, healthcare providers may experience unsustainable financial losses. These underpayments along with egregious denials are pushing providers to the limit.

In such cases, CFOs may weigh the option of contract termination as a last resort to protect the financial stability of the organization.

“There is rarely one final straw, but rather, a cumulation of events that negatively impact the fiscal viability of the relationship,” Britt Berrett, managing director and teaching professor at Brigham Young University and former CEO with HCA, Texas Health Resources, and SHARP Healthcare, explained.

“Long before rates become contentious, hospitals are dealing with bad behavior and payer shenanigans,” Berrett said.

For example, he says, payers are rejecting claims based on utilization review criteria. Many healthcare leaders consider these rejections to have little to do with utilization but rather an attempt to refuse payment.

Luckily for providers, organizations are becoming more capable of cost accounting and utilizing analytics to determine the actual cost by patient and payer.

Why Medicare Advantage?

Why has MA been in the hot seat of terminations? While not the only culprit of the turmoil, organizations have been fighting back against MA’s low reimbursement rates for years, and as Berrett said, maybe CFOs are finding no fiscal viability in the relationship with the payer.

One case in point is Scripps Health. Two medical groups within the system canceled their MA contracts for 2024 because of low reimbursement rates, denials, and administrative costs to manage high utilization and out of network care.

“We’re unfortunately on the vanguard of what I think is going to be a very ugly few years between hospitals and commercial insurance companies,” Chris Van Gorder, president and CEO of Scripps, told USA Today.

And Scripps has the resources to better manage these burdens, meaning these burdens are even more exacerbated for smaller systems.

An example of this is Samaritan Health Services. It recently terminated its commercial and MA contracts with UnitedHealthcare.

The five-hospital, nonprofit health system cited slow processing of requests and claims that have made it difficult to provide appropriate care to UnitedHealth's members, according to a news release from Samaritan.

“This, along with other factors, is not in alignment with our mission of building healthier communities together,” the health system said.

Another example is St. Charles Health System, a four-hospital network and healthcare company in Central Oregon, which terminated its MA contracts in 2023.

Steve Gordon, president and CEO of St. Charles, said great thought went into the decision to reevaluate MA participation, and it was done only after years of concerns piled up not just at St. Charles, but at health systems throughout the country.

“The reality of Medicare Advantage in central Oregon is that it just hasn’t lived up to the promise,” he said in a press release. “A program intended to promote seamless and higher quality care has instead become a fragmented patchwork of administrative delays, denials, and frustrations. The sicker you are, the more hurdles you and your care teams face. Our insurance partners need to do better, especially when nurses, physicians and other caregivers are reporting high levels of burnout and job dissatisfaction.”

It's also worth noting that Memorial Hermann Health System, the largest hospital system in the Houston region, terminated its agreement with Humana's MA networks at the beginning of the new year. Memorial Hermann has not yet publicly cited why, other than saying the contract negotiations hit an impasse.

OK, but what’s the outcome of termination?

But what is it like on the other side of an MA termination? It hasn’t been so bad for some.

Hamilton Health Care System, a not-for-profit, fully integrated system of care serving the northwest Georgia region, has been out of network with MA for years.

“We are not currently in network with any Medicare Advantage plans. We would end up netting less than traditional Medicare because of denials and administrative hassles,” said Julie Soekoro, EVP and CFO at Hamilton Health Care System.

In addition to a lessened administrative burden, being out of network hasn’t affected Hamilton’s bottom line or patient experience.

“Since we are out of network, the MA plan should be paying us as if the patient were a regular Medicare patient, so it has not affected the patients adversely,” Soekoro said.

All the time and money spent on takebacks, pre-authorizations, and denials add up. Coupled with the aforementioned low reimbursement rates, CFOs can find it doesn’t make business sense to continue with the payer.

MA isn’t the only difficult payer, though; the challenge is universal.

For example, Hamilton Health Care has spent a lot of time going back and forth on a contract with a national payer that wanted to bring them in network, only for Hamilton to walk away from the negotiation table.

“After spending a great deal of time and effort modeling the contract, we learned the payer will require all diagnostic imaging business to go to a freestanding competitor, while building in very attractive looking rates for imaging,” Soekoro said. “This is misleading in that they never intended to allow their subscribers to come to us for imaging.”

“This was discovered incidentally by our contracting director, rather than fully disclosed by the payer,” she added. “Also, certain provider-favorable terms that we built into the language have mysteriously fallen out of the most recent version of the language.”

As stated, Hamilton walked away from that particular negotiation.

Another example comes from Berrett and his time at Texas Health Resources.

While Berrett didn’t specify the type of plan (MA or otherwise), the organization terminated a payer contract because its patients had significantly higher CMI, resulting in losses for their patients.

“The impact [of terminating the contract] was very positive for the hospital. We lost volume but improved margins,” he said. “The payer was able to promote a significantly lower premium for companies because their rates to the providers were so low. When we terminated the agreement, they could no longer sell lower premiums and their market share dwindled. They eventually retreated from the market.”

What does the future hold?

It’s worth noting that the trend of MA terminations is not a common occurrence with the nation's health systems—yet. In fact, several health systems expanded their own 2024 MA subsidiaries.

But that hasn’t stopped the critiques of the program from growing louder.

The Health and Human Services Department’s inspector general reported last year that some MA plans have denied coverage for care that should have been provided under Medicare's rules. On top of this, CMS and the Biden Administration have both proposed rules to address certain aspects of the plan’s requirements.

Even so, the payer/provider relationship is sure to remain heated in the coming year—even beyond MA.

“At the same time that community hospitals are struggling to stay out of the red, the national payers are reporting profits in the billions in their quarterly earnings reports,” Soekoro said.

“It feels to me like the payers became accustomed to taking in premiums during the volume downturns of the COVID years when patients shied away from seeking follow through on regular—and sometimes even urgent—healthcare needs,” she said. “Now the payers seem to be looking for ways to sustain those increased quarterly earnings.”

As for the providers, CFOs could have more leverage in negotiation talks than they think, but it requires willingness and preparation to pull levers that may be uncomfortable yet necessary for financial survival.

Dropping a payer is “absolutely an important strategy,” Berrett says. “Providers are becoming more capable in measuring the impact of the slow or rejected payments, and providers are looking at the actual cost of care by patient. Payers need to be aware that.”

There are two important considerations for providers, Berrett says.

“Are we able to collect our negotiated rates, and are the patients covered by this payer more expensive to treat?”